EMI × Kohler · Marketplace Intelligence

Kohler Singapore

Home & Living Marketplace Review

Lazada & Shopee · January–April 2026

An executive synthesis of category performance, Kohler's competitive position, brand differentiation and the outlook — built from EMI's monthly decks and SKU-level marketplace data. Every figure is click-to-source.

Executive Summary · Market Size · Kohler Share · Trends & Platform · Growth vs Market · Competitive Landscape · Differentiation · 6-Month Outlook · Action Plan · Sources

01 · Executive Summary

The six things to know

- Kohler is rank #6 in Singapore — middle of pack in a premium-heavy field. ~6.4% share of the tracked sanitaryware competitive set over Jan–Apr, behind RIGEL (~28%), Grohe (~17%), Hansgrohe (~15%), Toto (~10%) and American Standard (~9%). This is a climb story, not a defend story — Kohler sits mid-table in a crowded premium field with no single mass-volume incumbent. source

- Kohler is gaining ground, but slowly. +1.24 share-points within the set Jan→Apr (+10% sales growth), while the major collapse came from RIGEL (−16.66pp share, −50% sales). Grohe meanwhile pulled away with +8.44pp share (+44% sales). The field is moving — Kohler held position but did not move with the leaders. source

- Pricing is anomalously low for a premium brand. Kohler's S$134 ASP is the lowest in the set — Grohe S$292, RIGEL S$348, Hansgrohe S$232, Toto S$611. Kohler sells broadly across price bands (39% <S$200, 23% S$700+), while rivals sit firmly above S$200. Premium positioning is not currently visible online in Singapore. source

- Channel discipline has room to tighten. 81% of Kohler sales are Official — solid, but the 19% grey-market leakage is real slippage for a premium brand. Tighter channel control is a structural edge not yet fully realised in Singapore. source

- Hero-SKU presence is thin. Just 1 Kohler product in the set's top-30 bestsellers (vs RIGEL 11, Toto 5, Grohe 4). Where Kohler does sell, it concentrates in Showers & Bidet Sprays — its strongest sub-category and a natural beachhead to build from. source

- RIGEL's collapse is the immediate opportunity. RIGEL lost half its sales (−16.66pp share), vacating premium demand worth ~S$180K/month. Kohler is well-positioned to capture some of this — but so are Grohe (gaining fastest, +8.44pp) and Toto (+6.75pp). Speed matters. source

- The real battle is the interior-designer channel, not just e-commerce. External research (Aissistance Deep Research) shows premium SG sanitaryware is gatekept by interior designers who control S$100k+ renovation budgets, and validated by B2B project specification (CDL, CapitaLand). Kohler already has the assets to win — the Kohler Experience Center and premium Statement/Anthem/Numi lines — but isn't connecting them to the ID workflow or its digital storefront. This reframes the action plan below.

02 · Market & Category Size

A SGD 10.6M category, premium-heavy and concentrated

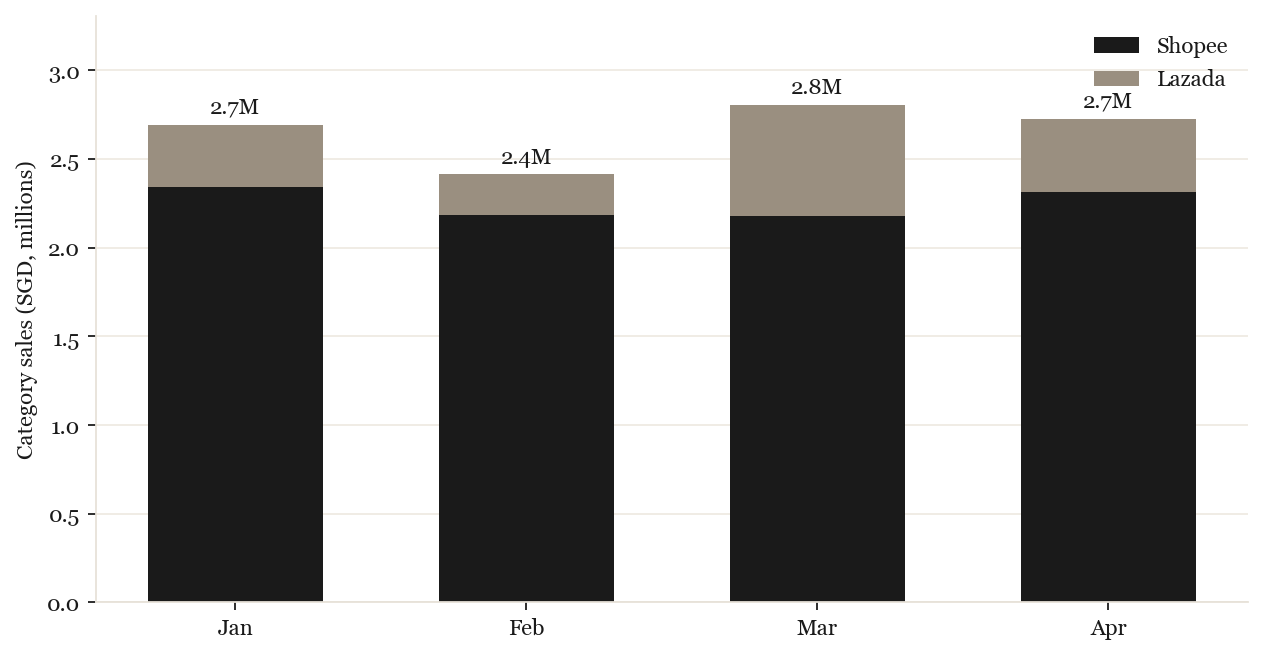

Singapore's Home & Living category on Lazada + Shopee turned over roughly SGD 10.6M in Jan–Apr 2026 (~SGD 2.4–2.8M per month). It is a premium-skewed market with no single mass-volume incumbent — demand is spread across a crowded field of established brands.

Of that total, ~36–44% is unbranded or off-core (jet sprays, sponges, faucet mats), so the real sanitaryware arena is much smaller: the tracked competitive set ran ~SGD 0.83–1.12M/month. This is the lens used throughout the rest of this report. source: deck source: data

Category sales by month, split by marketplace (all listings). Derived from EMI × Kohler SG raw data, Jan–Apr 2026.

03 · Kohler Market Share & Position

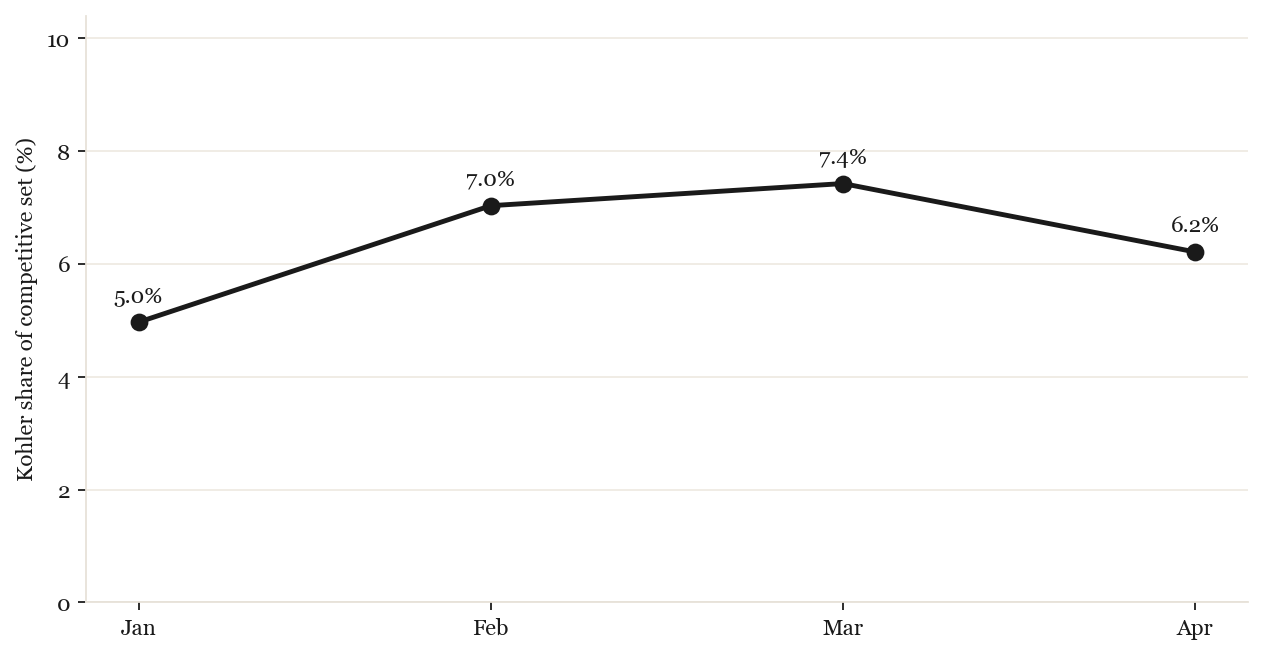

#6 in the arena — climbing modestly from a mid-pack base

Within the tracked sanitaryware set, Kohler rose from 4.97% (#6) in January to a 7.42% Mar peak, settling at 6.21% (#6) in April. Rank has been static — every month is #6 — behind a clear top five over the Jan–Apr period: RIGEL (~28%), Grohe (~17%), Hansgrohe (~15%), Toto (~10%) and American Standard (~9%). (Note: RIGEL is the established leader on a cumulative and moving-annual basis; Grohe edged ahead in the single month of April only, as RIGEL declined — see the momentum reshuffle below.) source

Among Official-store sales specifically, Kohler holds ~6.7% in April — broadly in line with its overall set share, indicating the brand is not yet over-indexed in the Official channel and has headroom to build a premium, brand-controlled position.

Kohler share of the tracked sanitaryware competitive set, by month. Scope & method: see RECONCILIATION.md.

04 · Category Trends & Platform

Shopee leads, but Lazada is a meaningful second channel

Shopee leads in Singapore, but the platform mix is relatively balanced. Lazada is a meaningful secondary channel — worth dedicated investment as a premium boutique, not just a holding pen. source

Platform split by month, Jan–Apr 2026 (all listings).

The longer view — 13-month trend & seasonality

The EMI deck's 13-month rolling trend shows the category running consistently above last year, with a Q1 build to a March peak and an April softening — a seasonal pattern, not a reversal. Singapore's renovation cycle (BTO completions, condo upgrades) and CNY-driven January spend both shape the rhythm. (Click the source tag to view the EMI deck's 13-month trend slide.) source

05 · Kohler vs Market Growth

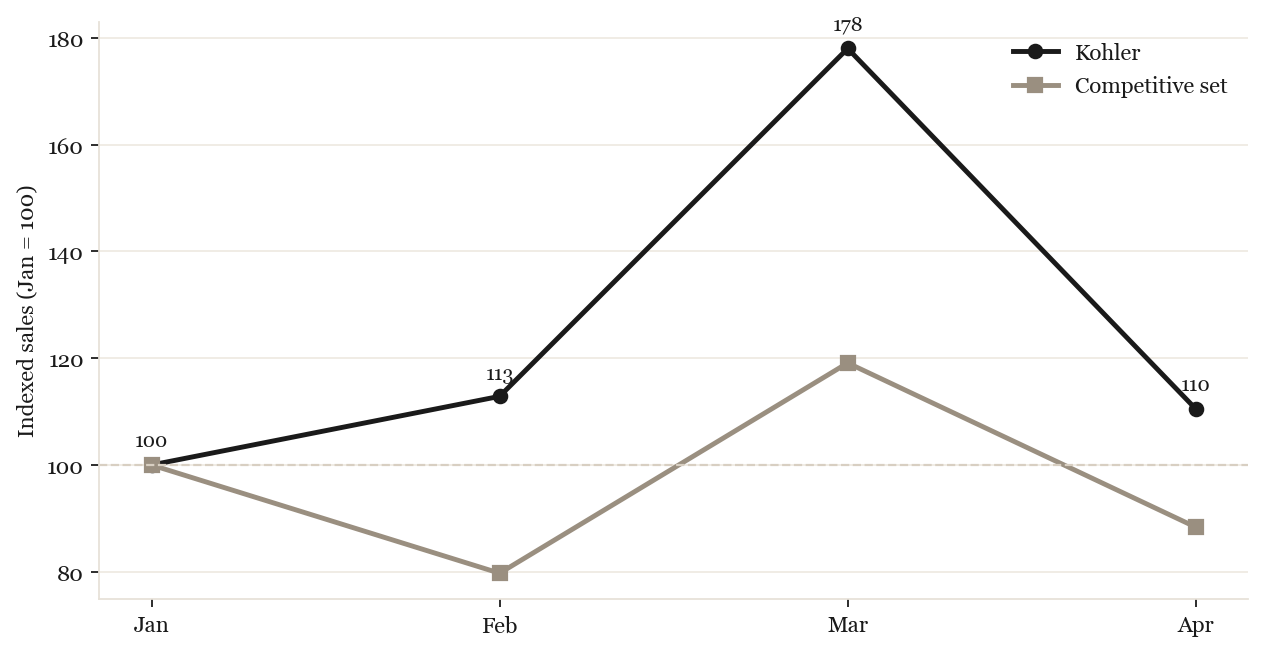

Holding position while the field reshuffles

The tracked set's total sales were down month-on-month in April (~SGD 0.83M vs SGD 1.12M in March, a seasonal dip), but the bigger story is the composition change: Grohe gained +8.44pp and RIGEL lost −16.66pp over the period — a major top-3 reshuffle Kohler didn't fully participate in. Kohler grew modestly (+1.24pp, +10% sales), enough to hold #6 but not to climb. source: deck source: data

Monthly sales indexed to January = 100, Kohler vs the competitive set.

06 · Competitive Landscape

RIGEL leads but is collapsing; Grohe closes in; Toto gains

RIGEL is the established leader — ~28% of the set over Jan–Apr (and clear #1 on the deck's moving-annual view) — but it is collapsing (−16.66pp, −50% sales), opening a major gap at the premium tier. Grohe (+8.44pp, +44% sales) is the fast-rising challenger, closing on RIGEL to the point of edging ahead in the single month of April; and Toto (+6.75pp, +89% sales) is climbing on its restocked one-piece toilet ranges. Hansgrohe softened (−4.41pp). Kohler's +1.24pp is modest in this context — the brand held without contesting the reshuffle. source

Competitive-set ranking — Jan–Apr (cumulative)

| Brand | YTD sales (S$K) | YTD share | Δ share (Jan→Apr momentum) |

|---|---|---|---|

| RIGEL | 1,005 | 27.6% | −16.7pp |

| Grohe | 602 | 16.5% | +8.4pp |

| Hansgrohe | 540 | 14.8% | −4.4pp |

| Toto | 364 | 10.0% | +6.7pp |

| American Standard | 333 | 9.1% | +3.0pp |

| Kohler | 234 | 6.4% | +1.2pp |

| Zuhne | 167 | 4.6% | +2.1pp |

| MEIDOO | 100 | 2.8% | +0.2pp |

Tracked sanitaryware set, cumulative Jan–Apr 2026 (ranked by total period sales; the Δ column shows within-period momentum). This ordering matches the EMI deck's moving-annual view, where RIGEL is #1. Untracked-but-material: Rubine (~SGD 73K in April), a credible local SG kitchen+bath brand outside EMI's tracking. Full Top-10 brand detail by platform is in the deck. Shopee Top 10 Lazada Top 10

What's winning — and what it reveals

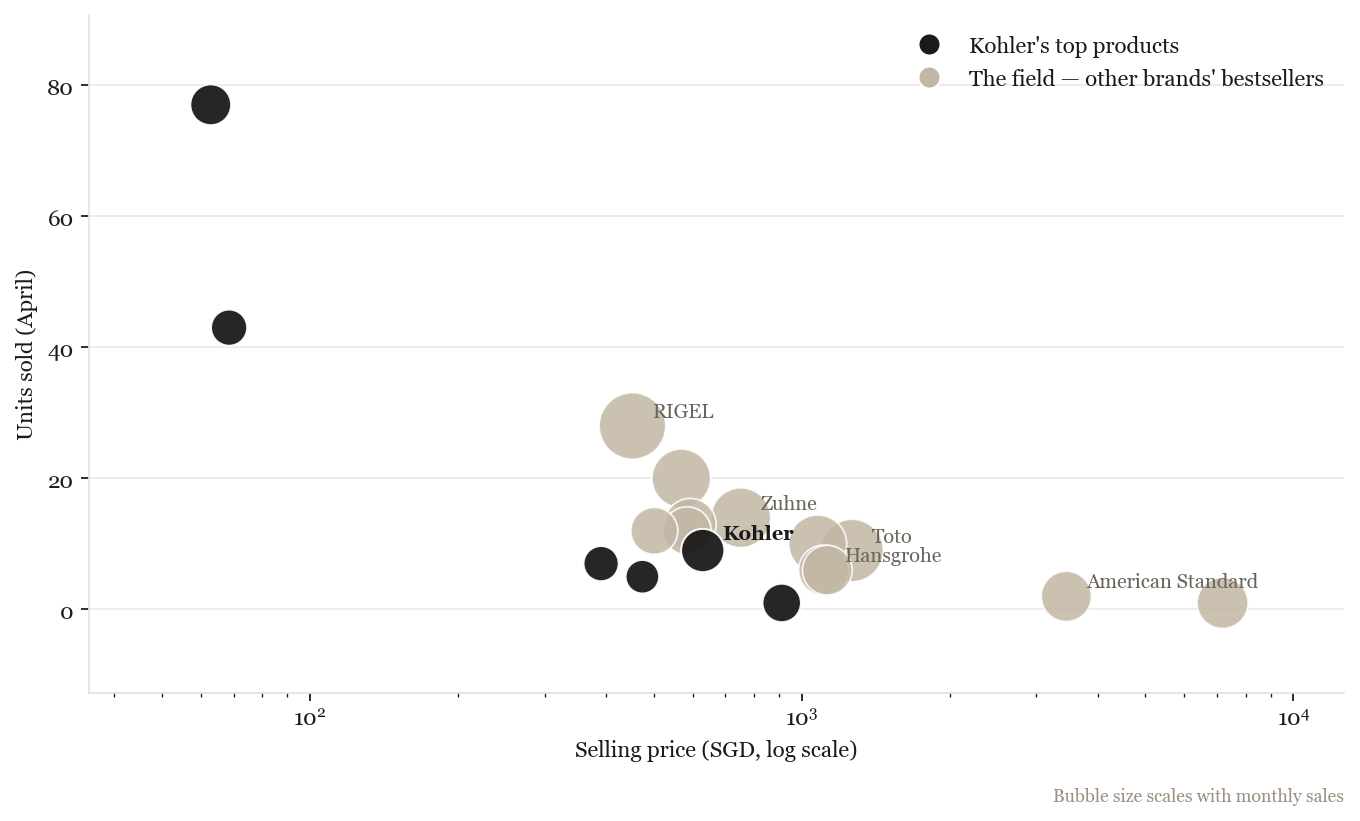

The bestseller list maps how each brand competes. RIGEL owns the list — 11 of the top 30 products, mostly premium toilets & shower sets despite its overall sales collapse, suggesting fewer-but-better SKUs. Toto (5), Grohe (4) and Zuhne (3) follow. Kohler has just 1 product in the top 30 — a clear gap in bestseller visibility. Where Kohler does sell, the heroes are kitchen fixtures, shower heads / hygiene sprays, and bathroom faucets — a diverse range, but thinly distributed with no breakout volume product. source deck SKUs

Kohler's bestsellers — kitchen, showers, scattered

Kohler's top 6 products spread across kitchen fixtures, shower heads, hygiene sprays and bathroom faucets — at price points from S$62 (hygiene spray, 77 units) to S$910 (premium shower set, 1 unit). Kohler's Singapore heroes are diverse but thin — spread across categories, with no single product moving significant volume.

| Kohler product (category L3) | Price S$ | Units | Sales S$ |

|---|---|---|---|

| Kitchen Fixtures (premium faucet) | 629 | 9 | 4,779 |

| Shower Head & Bidet Spray | 62 | 77 | 4,120 |

| Shower Head & Bidet Spray (premium) | 910 | 1 | 3,507 |

| Bathroom Fixtures | 68 | 43 | 2,961 |

| Kitchen Fixtures | 390 | 7 | 2,728 |

| Sinks & Taps | 474 | 5 | 2,371 |

07 · Brand Differentiation

Channel, sub-category, pricing

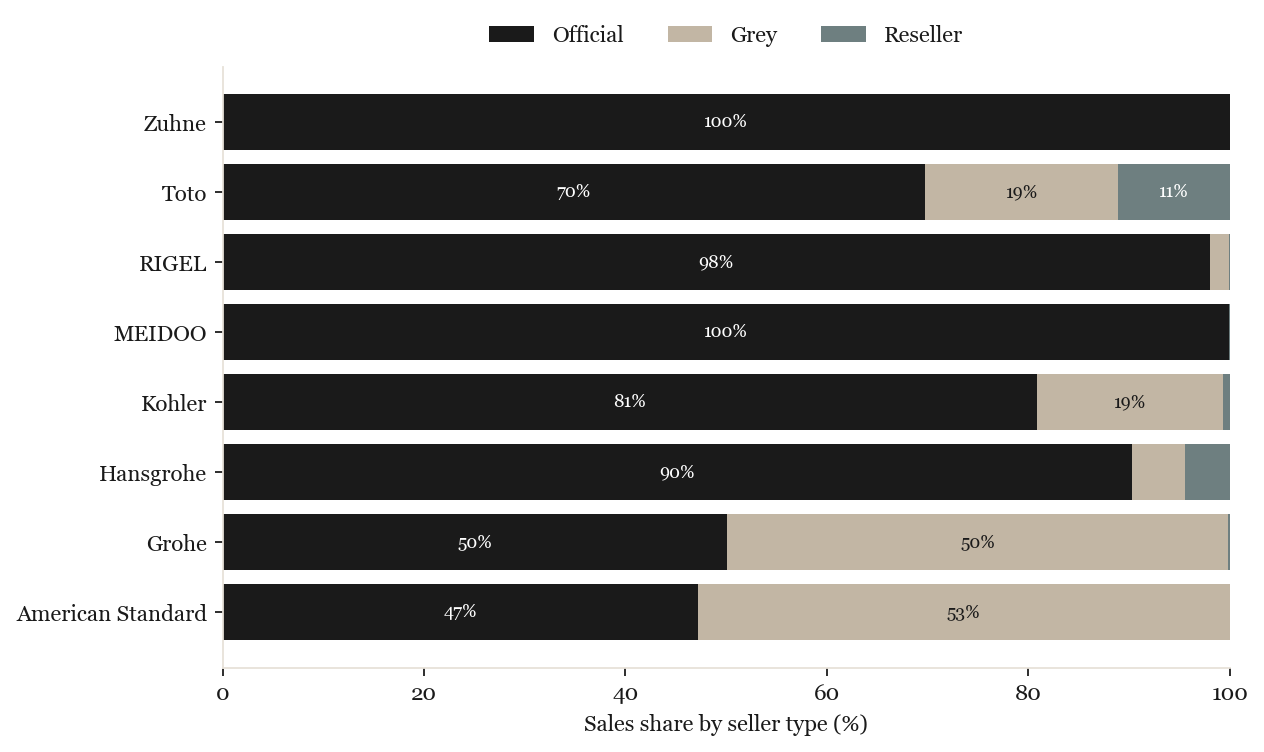

Channel — Official-led but with 19% grey leakage

81% of Kohler's sales flow through Official stores — solid, but the 19% grey-market share represents real channel-discipline slippage for a premium brand. By contrast, Hansgrohe runs ~90% Official and Zuhne/MEIDOO ~100%, while Grohe sits at just ~50% (half grey-market) and Toto ~70%. Kohler should be capable of matching Hansgrohe's discipline and closing that 19% gap. source

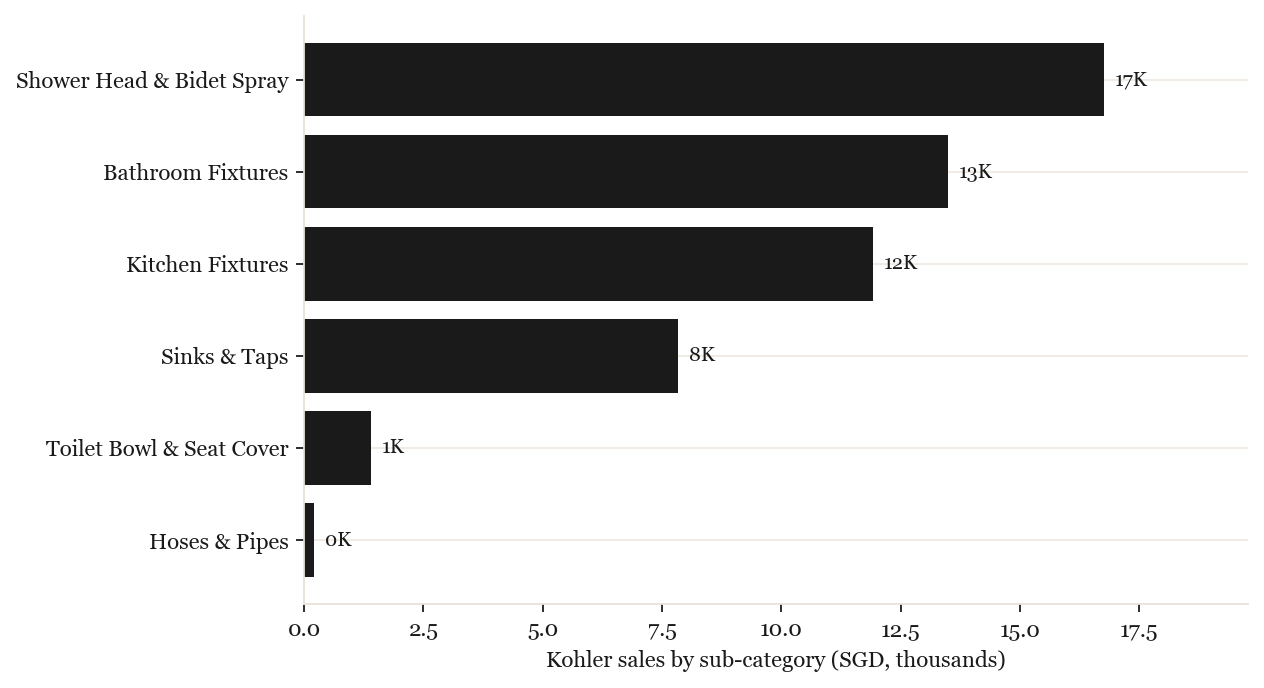

Where Kohler plays — showers, kitchen, bathroom — diversified

Kohler's Singapore sales are genuinely diversified across sub-categories: Shower Head & Bidet Spray (33%), Bathroom Fixtures (26%), Kitchen Fixtures (24%), Sinks & Taps (15%). Kitchen is a notable Singapore strength — over a quarter of Kohler's SG sales. Toilets are minor (~3%). source

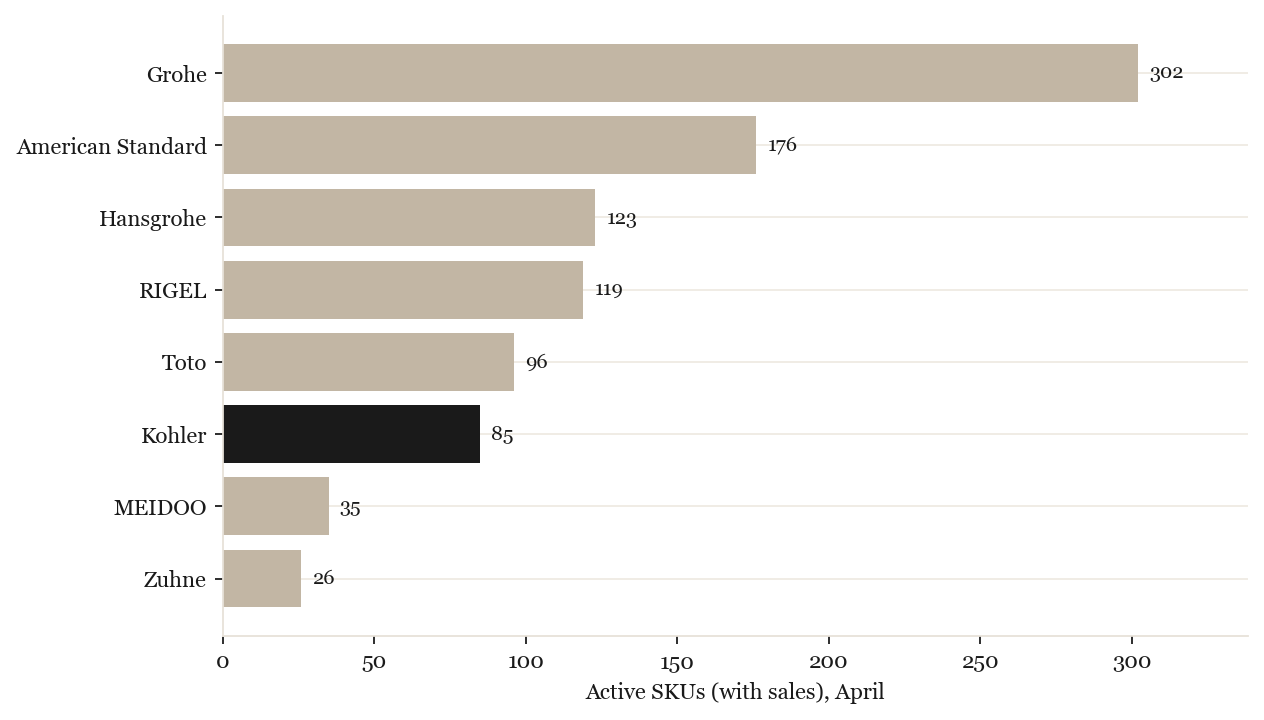

Assortment — focused 85 SKUs / 12 sellers

Kohler sells through just 85 active SKUs and 12 sellers in Singapore — mid-pack and notably narrower than the leaders. Grohe carries 302 active SKUs, American Standard 176, Hansgrohe 123 and RIGEL 119; Kohler (85) sits below Toto (96). Worth assessing: is 85 SKUs deliberate focus or insufficient shelf presence against a 300-SKU leader? source

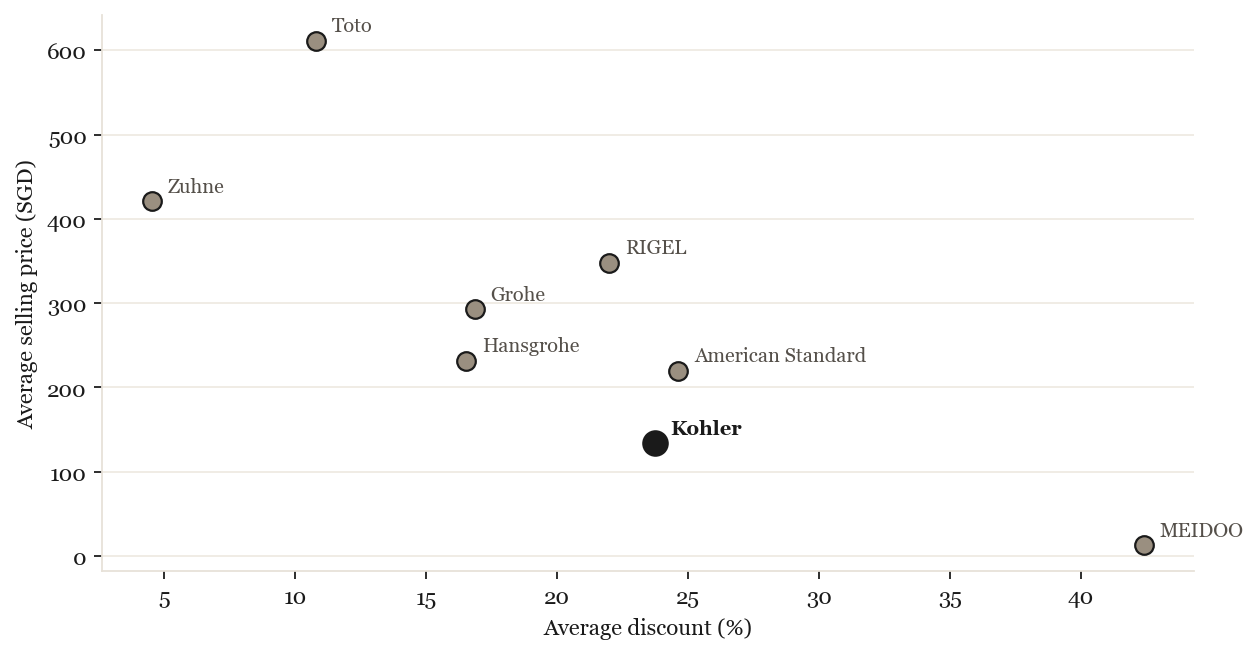

Pricing — anomalously low for a premium brand

Kohler's S$134 ASP is the lowest in the set — Grohe S$292, RIGEL S$348, Hansgrohe S$232, Toto S$611. Combined with 24% discount and 81% promotion-coverage, Kohler looks more like a mid-tier than a premium player in Singapore. Either the assortment skews to low-ticket accessories (sprays, S$60–134 items), or premium positioning needs reinforcing. source

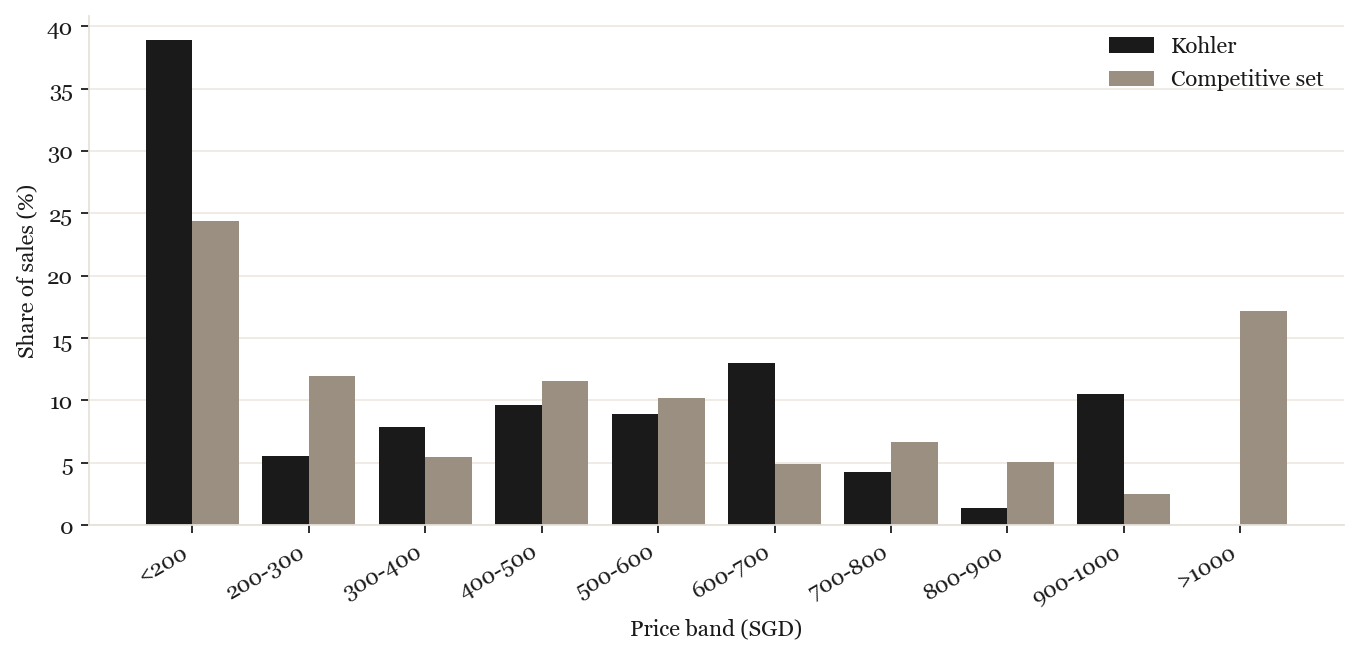

Price-band footprint — spread, not concentrated

Kohler's price-band distribution is unusually spread — 39% <S$200, 23% S$200–500, 22% S$500–700, 16% S$700+. The competitive set sits more decisively in higher bands (rivals Grohe / Toto / RIGEL have most of their volume S$200+). Kohler is the only set member with meaningful sub-S$200 presence — explaining the S$134 ASP and suggesting a positioning question. source

Promotion reliance — middle of pack, but real

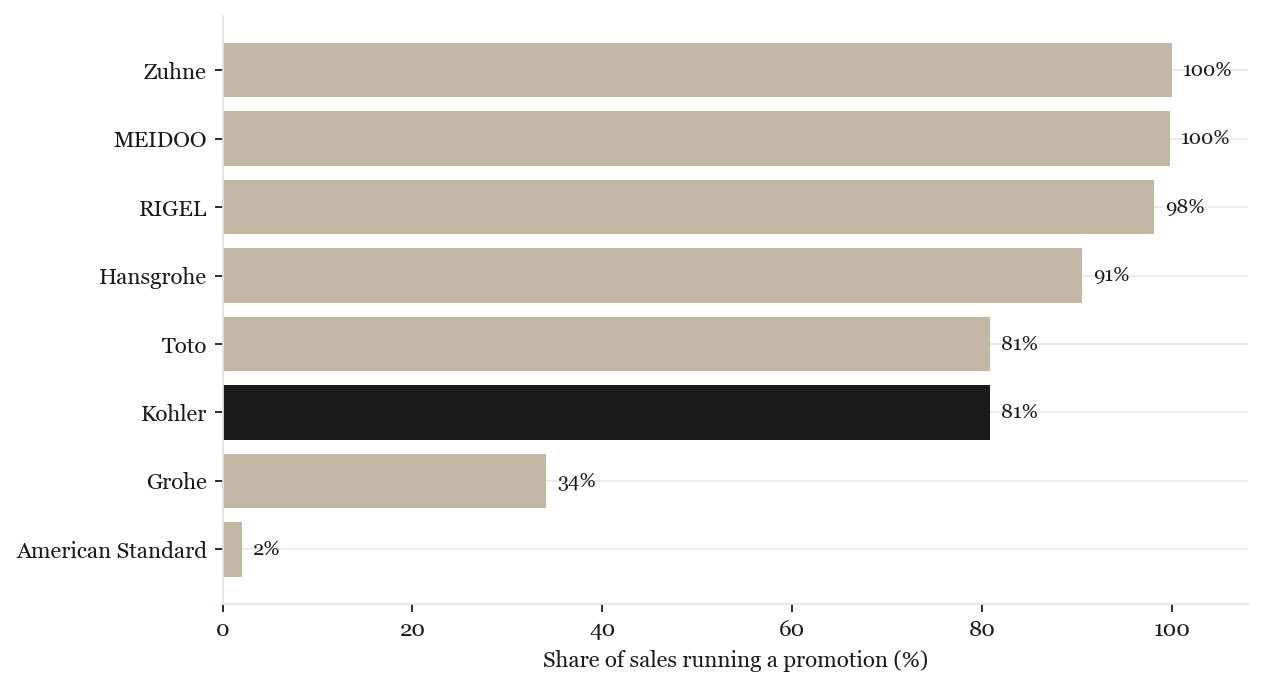

81% of Kohler's sales run on a promotion at a 24% average discount — middle of the set, well below Zuhne / MEIDOO / RIGEL (91–100% on promo) but above Grohe (34%) and far above American Standard (just 2% on promo). Kohler's promotional reliance is moderate, not extreme — but sustained discount dependence still erodes premium positioning over time. source

Listing quality — table stakes

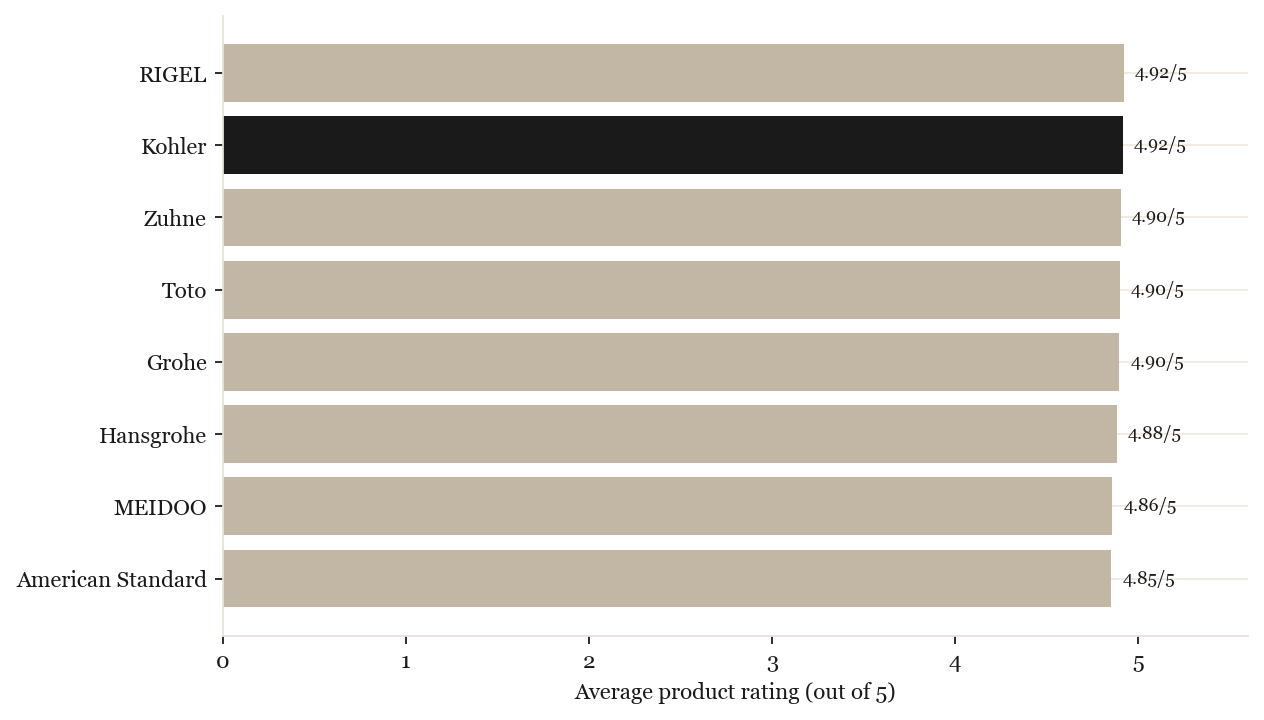

Every brand clusters around 4.9/5 on product ratings, so listing quality is a baseline expectation rather than a point of difference. source

08 · Six-Month Outlook

Where the next two quarters point

Directional calls grounded in the 4-month trajectory and the deck's 13-month seasonality. Ranges are indicative, not forecasts.

| Theme | Direction | Read |

|---|---|---|

| Category demand | →/↑ | Rebound from the April seasonal dip likely. SG renovation cycle (BTO completions, condo upgrades) supports steady premium demand. No structural decline visible. |

| Kohler set share | →/↑ | Hold-to-extend #6 with a plausible ~6–9% range if Kohler captures lapsed RIGEL/Hansgrohe premium share. Upside: pass American Standard (the brand directly above it, ~9%) to reach #5 within 2–3 quarters. |

| Competitive risk | watch | Grohe rising fast and closing on the declining RIGEL; Toto climbing on toilets; American Standard rebuilding (+3pp). Rubine outside tracked set but material. |

| Brand-positioning risk | watch | S$134 ASP and 39% sub-S$200 share mean Kohler reads as mid-tier in SG. If left unaddressed, this erodes the premium brand equity earned globally. |

Seasonality & long-horizon basis: EMI deck 13-month trend & MAT. source

External signals — forward-looking context

Surfaced by Aissistance Deep Research; treat as forward-looking signals rather than already-realised changes in our April data.

| Signal | Type | Read & implication for Kohler |

|---|---|---|

| Interior-designer (ID) channel controls premium specification | structural lever | IDs gatekeep S$100k+ reno material choices and favour reliable-supply brands (Grohe, Hansgrohe). Winning the ID channel (Action #9) is the single biggest structural lever in SG — bigger than any single e-commerce tactic. EXT ↗ |

| B2B project specification (CDL, CapitaLand, Frasers) | tailwind | Premium sanitaryware is specified before reaching consumers; landmark wins (e.g. CDL Newport) become 5-year demand-setters. Kohler should pull its luxury-hospitality placements into consumer-facing marketing. EXT ↗ |

| Competitor premium investment — Hansgrohe PVD finishes, AXOR designer nights | critical risk | Hansgrohe invested €5M in special-finish (bronze, matte black, gold) capacity and courts IDs with exclusive events; Toto owns smart-toilet Washlet mindshare. Kohler must match on finishes & designer relationships. EXT ↗ EXT ↗ |

| Discounting erodes equity in the SG premium market | watch | The affluent SG buyer reads deep promotion as a commodity signal. Sustained 24% discounting trains buyers to wait for sales — directly at odds with the climb-in-premium goal. EXT ↗ |

09 · AI Action Plan

Nine moves — marketplace data sharpened by external research

The marketplace data drove an initial climb plan; an external Aissistance Deep Research pass reframed the core strategy and surfaced three new channel-led fronts. The single biggest message: Singapore is a climb-in-premium game, won with price integrity, engineering proof and the interior-designer channel — not with promotion and volume. Heavy discounting here actively erodes equity.

1 · Climb past American Standard to #5

Kohler (#6, ~6.4%) trails American Standard (#5, ~9.1%) by ~2.7pp. Kohler is growing (+1.2pp) and can close the gap by capturing lapsed RIGEL/Hansgrohe premium share.2 · Counter RIGEL with heritage & wellness

RIGEL owns utilitarian reliability. Don't fight on utility — reposition on 150 years of design heritage and spa-wellness for the premium condo market. EXT ↗3 · Protect ASP with a platform-category split

Shopee for entry accessories to defend rank; LazMall for premium lines with zero flat discounting — stop training buyers to wait for the next sale. EXT ↗4 · Discounts → Gift-With-Purchase

Replace the 24% discount with high-margin GWP bundles (towel racks, soap dispensers) during Double-Date sales — satisfy the "deal" expectation without eroding the premium. EXT ↗5 · Lift ASP toward the premium tier

S$134 ASP is half Grohe's, a quarter of Toto's. Rebalance assortment up; the 11% of sales in S$900–1,000 proves premium sells.6 · Build hero SKUs in showers & bidet sprays

Already Kohler's #1 sub-category (33%); just 1 product in the set's top 30. Need 3–5 hero SKUs for bestseller visibility.7 · "Engineering Proof" content (Dyson playbook)

Shift PLPs from lifestyle imagery to physics: water-saving tech, finish durability, smart-toilet mechanics — justify the price to pragmatic SG buyers. EXT ↗8 · Digitise the Kohler Experience Center

Use the Peck Seah St KEC as a live-commerce studio (LazLive/Shopee Live); trigger "Book a private viewing" on high-ticket carts for O2O conversion. EXT ↗9 · Gated trade portal for interior designers

IDs gatekeep S$100k+ reno budgets. Offer registered IDs trade pricing, CAD/BIM files, priority logistics and WhatsApp support to build client carts in Kohler's ecosystem. EXT ↗Detail & rationale

- Climb past American Standard to #5. On a Jan–Apr basis Kohler is #6 (~6.4%), trailing American Standard at #5 (~9.1%) by ~2.7pp. Kohler is growing modestly (+1.2pp) while the declining leaders (RIGEL −16.7pp, Hansgrohe −4.4pp) shed premium share — focused execution to capture that demand is the path up the table. source

- Counter RIGEL with a "Heritage & Wellness" narrative — and capture its vacated demand. RIGEL lost ~S$180K/month and 16.7 share-points — the biggest opening in the set — but owns utilitarian, commercial-grade reliability. Kohler shouldn't compete on basic utility; reposition on 150 years of American design heritage and spa-like wellness, then conquest RIGEL's premium toilet/shower categories before Grohe and Toto sweep the rest. source EXT ↗ ID channel

- Protect ASP with a strict platform-category split. Halt uniform promotions. Use Shopee for entry-level, fast-moving accessories (basic showerheads, manual bidets) to defend rank and traffic; reserve LazMall for premium lines (Statement, Anthem, Numi) with zero flat-rate discounting. The sophisticated SG buyer reads blanket discounts as a signal the product is overpriced at MSRP. source EXT ↗

- Replace discounts with Gift-With-Purchase bundling. 81% of Kohler's SG sales run on a 24% promotion. Swap cash discounts for high-margin, aesthetically aligned GWP (premium towel racks, matching soap dispensers) bundled with primary WC/shower purchases during Double-Date sales — satisfies the deal expectation without destroying the S$134 ASP it should be lifting. source EXT ↗

- Lift average selling price toward the premium tier. Kohler's S$134 ASP is the lowest in the set (Grohe S$292, RIGEL S$348, Toto S$611). Rebalance assortment toward higher-ticket SKUs and prune low-end product; the 11% of sales already in the S$900–1,000 band proves premium sells. source source

- Build hero SKUs in Showers & Bidet Sprays. Already Kohler's #1 sub-category (33% of SG sales) and aligned with strong local hygiene-spray demand — yet just 1 Kohler product sits in the set's top 30. Concentrate launch and media support to build 3–5 genuine hero SKUs. source source

- Launch "Engineering Proof" content (the Dyson playbook). To climb from mid-pack in a mature affluent market, compete on physics, not price. Overhaul product pages from lifestyle imagery to technical, GIF-heavy demonstrations — water-saving mechanics, finish-durability testing, smart-toilet self-cleaning — to justify premium pricing to pragmatic SG buyers. EXT ↗

- Digitise the Kohler Experience Center for O2O conversion. Kohler already has the physical infrastructure — a three-storey KEC on Peck Seah Street with live Numi / DTV+ / VibrAcoustic displays. Use it as a live-commerce broadcast studio (LazLive / Shopee Live) and trigger a "Book a KEC private viewing" prompt on high-ticket carts to close with high-touch service. EXT ↗

- Build a gated e-commerce trade portal for interior designers. IDs are the gatekeepers of S$100k+ condo renovation budgets and favour brands with reliable supply, zero missing parts and strong local warranties. Offer registered IDs trade pricing, priority logistics, CAD/BIM downloads and direct WhatsApp support — incentivising them to build client carts inside Kohler's ecosystem. This is the highest-leverage structural move in the SG market. EXT ↗ EXT ↗

10 · Sources

Every insight, traced

Click any insight's "source" tag above, or any thumbnail below, to view the underlying slide or chart. Derived charts are computed from EMI × Kohler SG SKU-level data (Jan–Apr 2026, Lazada + Shopee); deck pages are from the EMI × Kohler SG April 2026 report.

External research

Aissistance Deep Research, 3-pass run (June 2026). Each item below links out to the cited source in a new tab.